Source: Stuart Eizenstat. President Carter - The White House Years (2018)

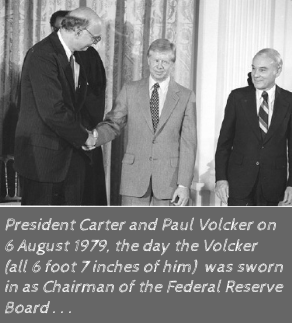

President Carter had no idea what he had started by asking Volcker if he could reduce the money supply without raising the Discount Rate and Volcker’s solution would be his contribution to US History. Volcker started to think about ways to attack market psychology using other tools directly and indirectly related to monetary policy, and like a general blocked in the field of battle in one direction, Volcker went in another direction.

Volcker concluded that he would never tame inflation by increasing the Discount Rate, so he had to find another way to reduce the money supply; in effect Volcker was trying to find a practical way to carry out Milton Friedman’s argument that all the Federal Reserve really needed to do was to control the money supply. Volcker decided to directly regulate the level of bank reserves and let the federal funds rate go where it went. The shake-up came in October 1979, in large part because Volcker wanted to show his two immediate predecessors that they were wrong in their argument that the Fed was not able to curb the current level and type of inflation. Volcker was determined to show that the Fed could not only slow down inflation, but actually decrease inflation.

On 6 October 1979, Volcker called an emergency meeting of the Open Market Committee, and with only two exceptions, the OMC endorsed Volcker’s new plan for the Fed to attack inflation. Basically, Volcker set a money supply target using the Fed’s ability to buy and sell government securities/bonds. Also, Volcker knew how to give himself and the Fed some political cover since technically the Fed wasn’t directly setting its sights on increasing interest rates, but regulating the money supply.

Volcker concluded that he would never tame inflation by increasing the Discount Rate, so he had to find another way to reduce the money supply; in effect Volcker was trying to find a practical way to carry out Milton Friedman’s argument that all the Federal Reserve really needed to do was to control the money supply. Volcker decided to directly regulate the level of bank reserves and let the federal funds rate go where it went. The shake-up came in October 1979, in large part because Volcker wanted to show his two immediate predecessors that they were wrong in their argument that the Fed was not able to curb the current level and type of inflation. Volcker was determined to show that the Fed could not only slow down inflation, but actually decrease inflation.

On 6 October 1979, Volcker called an emergency meeting of the Open Market Committee, and with only two exceptions, the OMC endorsed Volcker’s new plan for the Fed to attack inflation. Basically, Volcker set a money supply target using the Fed’s ability to buy and sell government securities/bonds. Also, Volcker knew how to give himself and the Fed some political cover since technically the Fed wasn’t directly setting its sights on increasing interest rates, but regulating the money supply.

Volcker knew the devil was in the details, and that there would be many hiccups between adjusting the bank reserves and adjusting the money supply; Volcker was banking that the emerging psychology would be that the Fed was perceived as being able to adjust the money supply, and hence inflation. Volcker admitted in 1979 that he had no idea when interest rates would peak as a result of his new Fed machinery. Short-term interest rates became more volatile than what was initially feared, and Volcker didn’t expect interest rates to go past 20% as they did in 1980 while America was still held hostage by Stagflation.

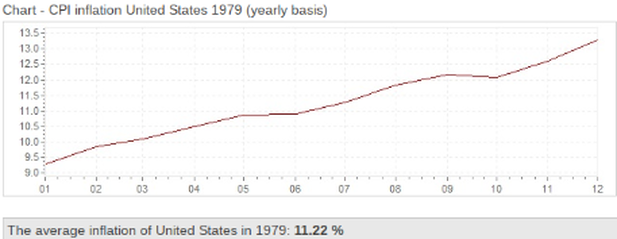

Carter, ever the Populist, was certainly not pleased, knowing that banks were making out like bandits with interest rates in the upper-teens while borrowing money from the Fed at interest rates at least six point lower. Carter wanted to know why the Prime Rate was at 19% while inflation was at 13%, but Volcker refused to relent. Carter wanted to show the US that Volcker wasn’t the only anti-inflation show in DC, and on 14 March 1980, Carter made yet another nationwide address on inflation. Carter tried to impose controls on consumer credit, which negatively affected Volcker’s approach and would exacerbate the recession. While it was true that consumers had reached a high level of debt, the idea to restrict consumer spending by restricting consumer credit to increase savings undermined the Fed’s program.

Carter, ever the Populist, was certainly not pleased, knowing that banks were making out like bandits with interest rates in the upper-teens while borrowing money from the Fed at interest rates at least six point lower. Carter wanted to know why the Prime Rate was at 19% while inflation was at 13%, but Volcker refused to relent. Carter wanted to show the US that Volcker wasn’t the only anti-inflation show in DC, and on 14 March 1980, Carter made yet another nationwide address on inflation. Carter tried to impose controls on consumer credit, which negatively affected Volcker’s approach and would exacerbate the recession. While it was true that consumers had reached a high level of debt, the idea to restrict consumer spending by restricting consumer credit to increase savings undermined the Fed’s program.

Volcker, in the worst possible way, didn’t want to venture into the world of directly limiting consumer credit even though he had the authority to do so. To Volcker, durable goods (e.g. cars and housing), the main objects of consumer credit, were exempt from the Fed’s plan for adjusting the money supply. But Volcker felt the pressure to go along with Carter’s plan since Carter had stayed true to his word and had stayed out of the Fed’s business.

But Volcker wanted to make the tightening of credit as minimal as possible, believing there was no actual consumer credit problem at all; it was another example in US History of politicians such as Carter not understanding economics. Carter even went so far as to preach to Americans that it was unpatriotic to use credit cards. Volcker feared that Carter’s plan would kill the momentum of the Fed’s plan, and soon and sure enough, consumption (consumer spending) fell off the table.

But Volcker wanted to make the tightening of credit as minimal as possible, believing there was no actual consumer credit problem at all; it was another example in US History of politicians such as Carter not understanding economics. Carter even went so far as to preach to Americans that it was unpatriotic to use credit cards. Volcker feared that Carter’s plan would kill the momentum of the Fed’s plan, and soon and sure enough, consumption (consumer spending) fell off the table.

Sales of big-ticket items fell 30% - 40%, and the Gross Domestic Product fell by 9%, which was the largest single drop in GDP in one quarter since the Great Depression. Volcker agreed that it was purely a psychological reaction to Carter’s credit policy, and interest rates went down which meant that the Fed had to inject money in the system to keep the economy from dropping any further . . . and when the dust settled, inflation increased even further. Volcker believed that Carter was getting far too many diverse and erroneous views from within his administration, taking him away from his basic instincts which was to be fiscally conservative.

But unlike Volcker, Carter had to work in the realities of his principles on the one hand and the interests of very powerful people/groups arrayed, in most cases, against him. The US economy grew at 3.3% under Carter, and 3.5% under Reagan. Carter never did achieve his dream of a balanced budget, but that was due more to a lack of revenue than too much government spending. But Carter’s message to the American people from the beginning of his Presidency was that of sacrifice and pain, which would prove to be a political liability in 1980, compared to Reagan’s message of hope and optimism.

But unlike Volcker, Carter had to work in the realities of his principles on the one hand and the interests of very powerful people/groups arrayed, in most cases, against him. The US economy grew at 3.3% under Carter, and 3.5% under Reagan. Carter never did achieve his dream of a balanced budget, but that was due more to a lack of revenue than too much government spending. But Carter’s message to the American people from the beginning of his Presidency was that of sacrifice and pain, which would prove to be a political liability in 1980, compared to Reagan’s message of hope and optimism.

Inheriting Stagflation and experiencing the shock of a second oil embargo in 1979, as well as a slowdown in production which to this day isn’t widely understood, Carter didn’t have much “economic luck” other than his choice of Volcker as Fed Chair. In retrospect, Carter should have acted far earlier in nominating Volcker as Fed Chair, but to be fair, Carter tried all he could on his end before he gave Volcker the ball to carry. Carter was the President that created the environment where the Federal Reserve changed how it approached adjusting the money supply related to inflation. In later years,

Volcker was very complimentary towards Carter, calling the former President courageous. Carter had the courage to make a tough decision that cost him politically, and even helped Reagan win re-election in 1984 in a historic landslide . . . but Carter’s decision to appoint Paul Volcker as Fed Chair has benefited the nation to this day.

Volcker was very complimentary towards Carter, calling the former President courageous. Carter had the courage to make a tough decision that cost him politically, and even helped Reagan win re-election in 1984 in a historic landslide . . . but Carter’s decision to appoint Paul Volcker as Fed Chair has benefited the nation to this day.