Source: Stuart Eizenstat. President Carter - The White House Years (2018)

On 24 October 1978, President Jimmy Carter made his fourth speech on inflation, pointing out that 6 million jobs had been created on his watch. Carter also stated that rising inflation was the nation’s main economic problem, and that inflation would get far more attention from his administration than unemployment. Carter introduced tougher wage and price controls to try and stop the vicious upwards spiral of inflation with no further tax cuts and more deregulation. Carter found himself in a race against time against businesses, Wall Street, and organized labor before they lost faith and confidence in his policies.

Despite Carter’s attempts to reduce inflation, the financial markets cast a vote of no confidence and the dollar dropped to an all time low in Asia, and then in Europe. During the first half of 1978, the dollar had lost 25% of its value against foreign currencies with inflation still raging. Normally the decline of the dollar would encourage sales abroad for US exports, but it also makes imports more expensive, in effect actually importing more inflation. Paul Volcker was the President of the Federal Reserve Bank of New York, and thereby in charge of the dollar in foreign currency markets. There was a link between inflation and the dollar, and Volcker was among the first to make that connection, even before Carter.

Despite Carter’s attempts to reduce inflation, the financial markets cast a vote of no confidence and the dollar dropped to an all time low in Asia, and then in Europe. During the first half of 1978, the dollar had lost 25% of its value against foreign currencies with inflation still raging. Normally the decline of the dollar would encourage sales abroad for US exports, but it also makes imports more expensive, in effect actually importing more inflation. Paul Volcker was the President of the Federal Reserve Bank of New York, and thereby in charge of the dollar in foreign currency markets. There was a link between inflation and the dollar, and Volcker was among the first to make that connection, even before Carter.

As the Congressional Elections of 1978 approached, inflation was rising while the dollar was decreasing. Carter issued a program that was to soon be called “Carter Bonds”, to address the problem that if the dollar did not rise, it would cost more money to repay nations w/ foreign currency. Markets in the US and abroad reacted positively, but the fact was that Carter was using a crutch to support the dollar compared to other currencies. Volcker wondered if it would be worth spending that kind of money to support the dollar when the day would soon arrive to repay the debt to the foreign bond holders.

By 1979, the dollar settled and the trade balance improved, but inflation was still a bear. What Carter showed was that the government needed to occasionally step in to correct currency markets. And it was becoming clearer to Carter (and Volcker) that with resistance from the various traditional Democratic bases, such as labor, a brutal monetary policy from the Federal Reserve would be the only solution to reduce inflation. Politically, that meant that

Senator Ted Kennedy (D; MA) would see Carter as vulnerable and he would pursue the Democratic nomination in 1980. Most economic experts forecast a recession during 1979, and it was in this political and economic landscape that Carter eventually decided to have the Fed reduce inflation using monetary policy, and the President was reviled for the correct decision.

By 1979, the dollar settled and the trade balance improved, but inflation was still a bear. What Carter showed was that the government needed to occasionally step in to correct currency markets. And it was becoming clearer to Carter (and Volcker) that with resistance from the various traditional Democratic bases, such as labor, a brutal monetary policy from the Federal Reserve would be the only solution to reduce inflation. Politically, that meant that

Senator Ted Kennedy (D; MA) would see Carter as vulnerable and he would pursue the Democratic nomination in 1980. Most economic experts forecast a recession during 1979, and it was in this political and economic landscape that Carter eventually decided to have the Fed reduce inflation using monetary policy, and the President was reviled for the correct decision.

During June 1979, inflation reached 11% and there were incredibly long lines for gas in America’s cities. Carter decided to cancel a planned speech on energy, and he retreated to Camp David, had a re-think, and then delivered what became known as the “Crisis of Confidence Speech” (a.k.a. the “Malaise Speech”; although he never used that word). Carter finally realized that it was time to replace the largely incompetent G. William Miller as Chairman of the Federal Reserve Board, and Volcker’s name was at the top of the list of nominees.

Volcker had already sent out signals that he would increase interest rates to attack inflation, and many in the Carter administration didn’t think Volcker would be a team player. VP Mondale was opposed to Volcker’s nomination, seeing recessioni likely during an Election Year, and that it would be bad politics with a Presidential Election the following year. Carter knew that the markets had confidence in Volcker, and Carter had reached the point where he knew his anti-inflation remedies had been useless . . . it was time for Volcker. Carter knew that unemployment would rise and there would be a recession, which would very likely doom his chances at re-election in 1980 since Democratic voters might abandon him in droves.

Volcker had already sent out signals that he would increase interest rates to attack inflation, and many in the Carter administration didn’t think Volcker would be a team player. VP Mondale was opposed to Volcker’s nomination, seeing recessioni likely during an Election Year, and that it would be bad politics with a Presidential Election the following year. Carter knew that the markets had confidence in Volcker, and Carter had reached the point where he knew his anti-inflation remedies had been useless . . . it was time for Volcker. Carter knew that unemployment would rise and there would be a recession, which would very likely doom his chances at re-election in 1980 since Democratic voters might abandon him in droves.

On 24 July 1979, Carter invited Volcker to the Oval Office. From Volcker’s perspective, the meeting didn’t go well with Carter (and Chairman of the Fed Miller), since he did all the talking and wasn’t very pleasant, whereas Carter was nothing put polite and attentive. Volcker told friends that he had blown the interview advocating a much tougher monetary policy. Volcker also told Carter that if he was Fed Chair, he wouldn’t want any White House interference, and if that was the case, he wouldn’t accept the position. But as always, Carter thought of what was good for the nation instead of what was good for him politically, even if it meant losing in 1980.

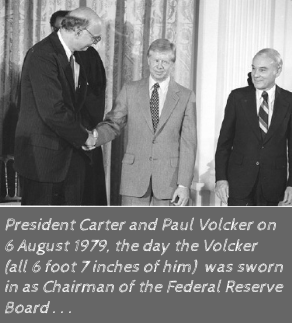

A few days later, Carter called Volcker and told him he would be the next Chairman of the Federal Reserve Board, and Volcker was sworn in on 6 August 1979. Carter kept his word and and let Volcker and the Fed do their thing, which was incredibly tough for the micromanaging Carter to do. Volcker saved the nation from economic disaster, and it was another example of Carter not receiving credit for doing the right thing. Reagan was lauded for standing behind Volcker in the face of Republican resistance on tight monetary policy, but Carter, the President that nominated Volcker, has not been properly credited.

A few days later, Carter called Volcker and told him he would be the next Chairman of the Federal Reserve Board, and Volcker was sworn in on 6 August 1979. Carter kept his word and and let Volcker and the Fed do their thing, which was incredibly tough for the micromanaging Carter to do. Volcker saved the nation from economic disaster, and it was another example of Carter not receiving credit for doing the right thing. Reagan was lauded for standing behind Volcker in the face of Republican resistance on tight monetary policy, but Carter, the President that nominated Volcker, has not been properly credited.

Ironically, Volcker didn’t come to the Fed with a clear blueprint of how to change the operating philosophy of the Fed, and he wasn’t a closet monetarist. Milton Friedman was the purist, and he was consistently scathing in his editorials about the Fed, even when Volcker became Fed Chair. But Friedman’s background was in the world of academia, while Volcker had worked his way up in the world of finance, and Volcker understood that the role of the Fed was that of central banking. In other words, the beyond-legendary Milton Friedman was a theorist, while Volcker was a pragmatist, believing that theorists such as Friedman didn’t have an idea how to break out of not only Stagflation, but the psychology of inflation.

Volcker issued a half-point rise in the Fed’s Discount Rate, but short-term interest rates remained unchanged; by not responding to the increase, the signal was sent by the financial sector that it had lost confidence in the Federal Reserve. Volcker again raised the Discount Rate another half-point to a record 11% on 18 September 1979, but the response was that the price of gold increased. Since the Federal Reserve Board’s vote was 4 - 3 on raising the Discount Rate, conventional wisdom was that Volcker and the Fed had shot their last bow from their quiver. Carter asked Volcker if there was a way to reduce the money supply without raising further raising the Discount Rate, and Volcker went home and tried to think of alternative methods; Volcker’s solution would change how the Federal Reserve operated, and would finally bring inflation back down to normal levels.

Volcker issued a half-point rise in the Fed’s Discount Rate, but short-term interest rates remained unchanged; by not responding to the increase, the signal was sent by the financial sector that it had lost confidence in the Federal Reserve. Volcker again raised the Discount Rate another half-point to a record 11% on 18 September 1979, but the response was that the price of gold increased. Since the Federal Reserve Board’s vote was 4 - 3 on raising the Discount Rate, conventional wisdom was that Volcker and the Fed had shot their last bow from their quiver. Carter asked Volcker if there was a way to reduce the money supply without raising further raising the Discount Rate, and Volcker went home and tried to think of alternative methods; Volcker’s solution would change how the Federal Reserve operated, and would finally bring inflation back down to normal levels.